DURATION function

The DURATION function is one of the financial functions. It is used to calculate the Macaulay duration of a security with an assumed par value of $100.

Syntax

DURATION(settlement, maturity, coupon, yld, frequency, [basis])

The DURATION function has the following arguments:

| Argument | Description |

|---|---|

| settlement | The date when the security is purchased. |

| maturity | The date when the security expires. |

| coupon | The annual coupon rate of the security. |

| yld | The annual yield of the security. |

| frequency | The number of interest payments per year. The possible values are: 1 for annual payments, 2 for semiannual payments, 4 for quarterly payments. |

| basis | The day count basis to use, a numeric value greater than or equal to 0, but less than or equal to 4. It is an optional argument. The possible values are listed in the table below. |

The basis argument can be one of the following:

| Numeric value | Count basis |

|---|---|

| 0 | US (NASD) 30/360 |

| 1 | Actual/actual |

| 2 | Actual/360 |

| 3 | Actual/365 |

| 4 | European 30/360 |

Notes

Dates must be entered by using the DATE function.

How to apply the DURATION function.

Examples

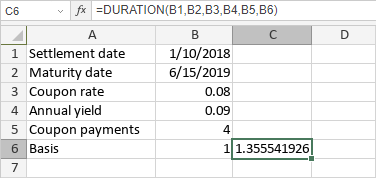

The figure below displays the result returned by the DURATION function.

Article with the tag:

Browse all tags